| 看看貸款計算的標準說法 |

| 送交者: suibian2009 2012年11月21日17:58:05 於 [五 味 齋] 發送悄悄話 |

|

http://en.wikipedia.org/wiki/Mortgage_calculator

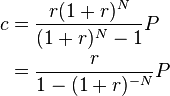

Monthly payment formula The fixed monthly payment for a fixed rate mortgage is the amount paid by the borrower every month that ensures that the loan is paid off in full with interest at the end of its term. The monthly payment formula is based on the annuity formula. The monthly payment c depends upon:

In the standardized calculations used in the United States, c is given by the formula:[1]  For example, for a home loan for $200,000 with a fixed yearly interest rate of 6.5% for 30 years, the principal is  The following derivation of this formula illustrates how fixed-rate mortgage loans work. The amount owed on the loan at the end of every month equals the amount owed from the previous month, plus the interest on this amount, minus the fixed amount paid every month. This fact results in the debt schedule: Amount owed at initiation: Amount owed after 1 month: Amount owed after 2 months: Amount owed after 3 months: Amount owed after N months: The polynomial  Applying this fact about cyclotomic polynomials to the amount owed at the end of the Nth month gives (using  The amount of the monthly payment at the end of month N that is applied to principal paydown equals the amount c of payment minus the amount of interest currently paid on the pre-existing unpaid principal. The latter amount, the interest component of the current payment, is the interest rate r times the amount unpaid at the end of month N–1. Since in the early years of the mortgage the unpaid principal is still large, so are the interest payments on it; so the portion of the monthly payment going toward paying down the principal is very small and equity in the property accumulates very slowly (in the absence of changes in the market value of the property). But in the later years of the mortgage, when the principal has already been substantially paid down and not much monthly interest needs to be paid, most of the monthly payment goes toward repayment of the principal, and the remaining principal declines rapidly. The borrower's equity in the property equals the current market value of the property minus the amount owed according to the above formula. With a fixed rate mortgage, the borrower agrees to pay off the loan completely at the end of the loan's term, so the amount owed at month N must be zero. For this to happen, the monthly payment c can be obtained from the previous equation to obtain:  which is the formula originally provided. This derivation illustrates three key components of fixed-rate loans: (1) the fixed monthly payment depends upon the amount borrowed, the interest rate, and the length of time over which the loan is repaid; (2) the amount owed every month equals the amount owed from the previous month plus interest on that amount, minus the fixed monthly payment; (3) the fixed monthly payment is chosen so that the loan is paid off in full with interest at the end of its term and no more money is owed. |

, the monthly interest rate is

, the monthly interest rate is  , the number of monthly payments is

, the number of monthly payments is  , the fixed monthly payment equals $1264.14. This formula is provided using the financial functionPMTin a

, the fixed monthly payment equals $1264.14. This formula is provided using the financial functionPMTin a

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

appearing before the fixed monthly payment c (with

appearing before the fixed monthly payment c (with  ) is called a

) is called a  because all but the first and last terms in this difference cancel each other out. Therefore, solving for

because all but the first and last terms in this difference cancel each other out. Therefore, solving for  yields the much simpler

yields the much simpler  to succinctly denote the function value

to succinctly denote the function value

|

|

|

| 實用資訊 | |

|

|

| 一周點擊熱帖 | 更多>> |

| 一周回復熱帖 |

| 歷史上的今天:回復熱帖 |

| 2011: | 建議右派小朋友們把巴二胡開除到垃圾堆 | |

| 2011: | 俺也侃兩句志願軍 | |

| 2010: | 孟什維克:苦難教會人類什麼東西? | |

| 2010: | 謙虛地問問:在光速火車上射出的光是否 | |

| 2009: | ZT上海閔行區現暴力拆遷 女戶主用燃燒 | |

| 2009: | 第一次在英國配眼鏡 | |

| 2008: | 老本:組群意識——華人與黑人很不同 | |

| 2008: | 突然有個問題.被執行的死刑的囚犯,可以 | |

| 2007: | 唯恐天下不亂 | |

| 2007: | 海鷗與電線杆子 | |